India’s digital payments ecosystem has undergone a dramatic transformation over the past decade. What began as a push toward cashless transactions has evolved into a sophisticated, always-on financial infrastructure that powers everything from daily purchases to long-term financial commitments. At the heart of this transformation lies the rise of recurring payments—automated transactions that eliminate the need for manual intervention and ensure seamless continuity for both businesses and consumers.

From streaming subscriptions and SaaS platforms to insurance premiums and loan EMIs, recurring payments have become the backbone of modern financial behavior. However, despite the convenience, one persistent challenge continues to plague businesses: payment failures. These failures not only disrupt services but also lead to involuntary churn, revenue leakage, and poor customer experiences.

To address this, two major systems have emerged as dominant players in India’s recurring payment landscape: UPI Autopay and eNACH. Both systems are designed to automate payments, but they differ significantly in terms of infrastructure, usability, transaction limits, reliability, and cost.

So, which one truly wins in 2026?

The answer isn’t as straightforward as picking a single winner. Instead, it depends on how well each system aligns with specific use cases, transaction sizes, and business priorities. This comprehensive guide breaks down UPI Autopay vs eNACH in detail, helping you understand where each excels and how to choose the right solution—or combination—for your needs.

The Rise of Recurring Payments in India

India’s subscription economy is booming. Consumers today expect convenience, automation, and flexibility. Whether it’s a ₹199 OTT subscription or a ₹75,000 monthly EMI, users no longer want to remember payment dates or deal with manual transactions.

For businesses, recurring payments offer predictable revenue streams, improved cash flow, and better customer retention. But they also introduce operational complexities—especially when payments fail due to insufficient balance, technical issues, or user friction during setup.

Traditional manual payment systems can see failure rates as high as 20–30%. This has made automated payment mandates not just a convenience, but a necessity.

Enter UPI Autopay and eNACH.

Understanding UPI Autopay

UPI Autopay is a recurring payment feature built on India’s real-time payment infrastructure. It allows users to authorize automatic debits directly through their UPI apps using a Virtual Payment Address (VPA).

Key Features

- Instant mandate creation: Users approve mandates in real time using their UPI PIN.

- Mobile-first experience: Entire flow happens within the UPI app.

- Flexible billing cycles: Supports daily, weekly, monthly, and even on-demand payments.

- Variable amount support: Merchants can debit different amounts within a predefined cap.

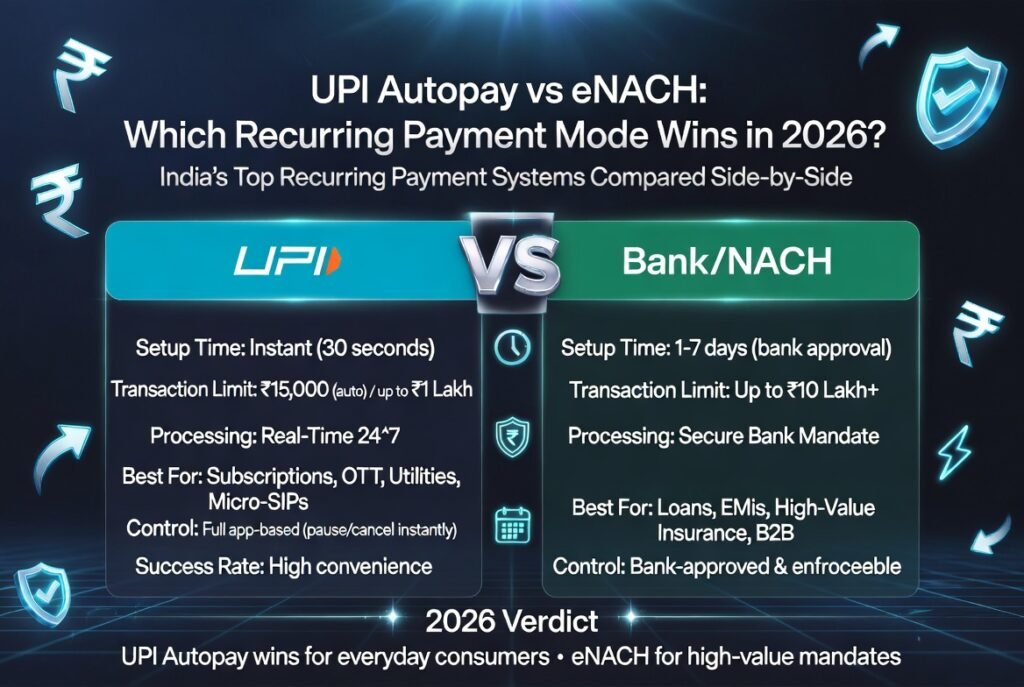

Transaction Limits (2026)

- Up to ₹15,000 per transaction without additional authentication

- Up to ₹1 lakh for select categories such as SIPs, insurance, and IPOs

Ideal Use Cases

- OTT subscriptions

- SaaS tools

- Utility payments

- Micro-investments

- Memberships and donations

UPI Autopay is designed for speed, convenience, and user control. It is particularly effective in high-volume, low-ticket scenarios where frictionless onboarding is critical.

Understanding eNACH

eNACH (Electronic National Automated Clearing House) is a bank-driven system that facilitates recurring payments through direct debit mandates.

It is the digital evolution of the traditional NACH system, replacing physical forms with electronic authentication.

Key Features

- Bank-to-bank processing: Operates through structured banking channels

- Multiple authentication methods: Netbanking, debit card OTP, Aadhaar-based verification

- High transaction limits: Suitable for large-value payments

- Batch processing: Transactions are processed in bulk through clearing cycles

Transaction Limits

- Up to ₹10 lakh per e-mandate

- ₹1 crore or more for paper-based NACH

Ideal Use Cases

- Loan EMIs

- Insurance premiums

- Education fees

- Corporate payments

- High-value subscriptions

eNACH is built for reliability and scale, making it the preferred choice for institutions and high-value transactions.

UPI Autopay vs eNACH: Head-to-Head Comparison

1. User Experience and Setup

UPI Autopay offers a seamless, app-based experience. Users receive a notification, review mandate details, and approve with a PIN—all within seconds.

eNACH, on the other hand, involves redirects to bank portals, credential entry, and OTP verification. This process can feel cumbersome, especially on mobile devices.

Verdict: UPI Autopay wins on user experience and conversion rates.

2. Activation Speed

UPI Autopay mandates are activated instantly. Businesses can start billing immediately.

eNACH mandates require bank validation, which can take anywhere from T+1 to T+7 days.

Verdict: UPI Autopay is significantly faster.

3. Transaction Limits

UPI Autopay is capped at ₹15,000 (standard) and ₹1 lakh (select categories).

eNACH supports much higher limits, making it suitable for large financial commitments.

Verdict: eNACH dominates in high-value transactions.

4. Reliability and Success Rates

UPI Autopay depends on real-time infrastructure. While fast, it can be affected by server downtime or peak traffic.

eNACH uses batch processing through banking systems, offering consistent reliability for bulk transactions.

Verdict: eNACH is more reliable for ongoing debits.

5. Flexibility

UPI Autopay supports a wide range of frequencies, including daily and on-demand billing.

eNACH is more rigid, with limited flexibility and difficulty in modifying mandates.

Verdict: UPI Autopay offers greater flexibility.

6. Cancellation and Control

UPI Autopay gives users full control. They can pause or cancel mandates directly from their app.

eNACH cancellations are more complex and may require bank or merchant intervention.

Verdict: UPI Autopay is more consumer-friendly.

7. Cost Structure

UPI Autopay generally has lower transaction costs and minimal setup fees.

eNACH involves higher processing costs and potential bounce charges for failed payments.

Verdict: UPI Autopay is more cost-effective for businesses.

Real-World Performance in 2026

UPI Autopay has seen explosive growth, driven by increasing adoption of digital services and mobile-first behavior. It has become the go-to solution for subscription-based businesses.

eNACH continues to dominate in sectors like banking, insurance, and education, where transaction sizes are large and reliability is critical.

Rather than competing directly, both systems are increasingly being used together in hybrid payment strategies.

When Should You Choose UPI Autopay?

UPI Autopay is the right choice if:

- Your transaction size is below ₹1 lakh

- You prioritize quick onboarding and high conversion rates

- Your customers are primarily retail users

- You offer flexible or usage-based billing

- You want lower operational costs

It is especially effective for startups, digital platforms, and consumer-facing services.

When Should You Choose eNACH?

eNACH is better suited if:

- Your transaction size exceeds ₹50,000 regularly

- Payment reliability is critical

- You operate in regulated industries

- You deal with corporate or institutional clients

- You require high-value mandate support

It remains the backbone of traditional financial systems.

The Hybrid Approach: Best of Both Worlds

In 2026, the smartest businesses are not choosing between UPI Autopay and eNACH—they are using both.

A hybrid strategy allows businesses to:

- Use UPI Autopay for onboarding and low-value transactions

- Switch to eNACH for high-value or long-term commitments

- Reduce payment failures through fallback mechanisms

- Optimize costs and user experience simultaneously

This approach can improve collection efficiency by up to 20% and significantly reduce churn.

Challenges and Limitations

UPI Autopay

- Limited transaction caps

- Dependency on real-time infrastructure

- Not widely supported for corporate accounts

eNACH

- Slower activation

- Higher setup friction

- Less user control

Understanding these limitations is crucial for making informed decisions.

Future Outlook

The future of recurring payments in India is likely to be shaped by:

- Increased UPI limits and capabilities

- Improved reliability of real-time systems

- Greater adoption of hybrid payment models

- Enhanced user control and transparency

- Integration with global payment systems

As technology evolves, the gap between UPI Autopay and eNACH may narrow—but their core strengths will remain distinct.

Final Verdict: Which One Wins?

There is no single winner in the UPI Autopay vs eNACH debate.

- UPI Autopay wins in speed, user experience, flexibility, and cost efficiency.

- eNACH wins in transaction limits, reliability, and institutional robustness.

The real winner is the business or consumer who chooses the right tool for the right job.

Conclusion

Recurring payments are no longer optional—they are essential. As India’s digital economy continues to expand, the need for reliable, efficient, and user-friendly payment systems will only grow.

UPI Autopay and eNACH represent two sides of the same coin: one optimized for the digital-first consumer, the other built for financial stability and scale.

In 2026, success lies not in choosing one over the other, but in understanding how to leverage both effectively. Businesses that adopt a hybrid approach will be better positioned to reduce failures, improve customer satisfaction, and maximize revenue.

Whether you’re a startup launching a subscription service or a financial institution managing large-scale collections, the key is simple: align your payment strategy with your business model—and let the technology do the rest.

FAQs

1. Can UPI Autopay replace eNACH completely?

No. Due to transaction limits and infrastructure differences, UPI Autopay cannot fully replace eNACH, especially for high-value payments.

2. Is UPI Autopay safe?

Yes. It uses secure authentication methods like UPI PIN and operates within regulated frameworks.

3. Why do eNACH payments sometimes fail?

Failures can occur due to insufficient balance, incorrect mandate details, or bank processing issues.

4. Can businesses use both systems together?

Yes. Many payment platforms support both, enabling hybrid strategies.

5. Which is better for startups?

UPI Autopay is generally better for startups due to its ease of use, quick setup, and lower costs.

By understanding the strengths and limitations of both systems, you can make smarter decisions and build a more resilient payment strategy in 2026 and beyond.