1. Introduction

In the sophisticated landscape of Indian banking, IFSC (Indian Financial System Code) and MICR (Magnetic Ink Character Recognition) serve as the fundamental pillars of transaction routing. While they may appear to the average user as a cryptic string of characters, as a fintech strategist, I view them as the “digital and magnetic addresses” of a bank branch. These unique identifiers, regulated by the Reserve Bank of India (RBI), are the guardians of your funds, ensuring every rupee reaches the correct destination without manual friction.

Understanding these codes is not just a matter of compliance; it is the key to secure, high-speed banking. Whether you are initiating an instant digital transfer or depositing a physical cheque, these codes provide the necessary authentication to keep the financial ecosystem moving.

👉 You can quickly find bank name, branch address, and MICR code using our IFSC tool: ifsc.arjunwatchandmobile.com

——————————————————————————–

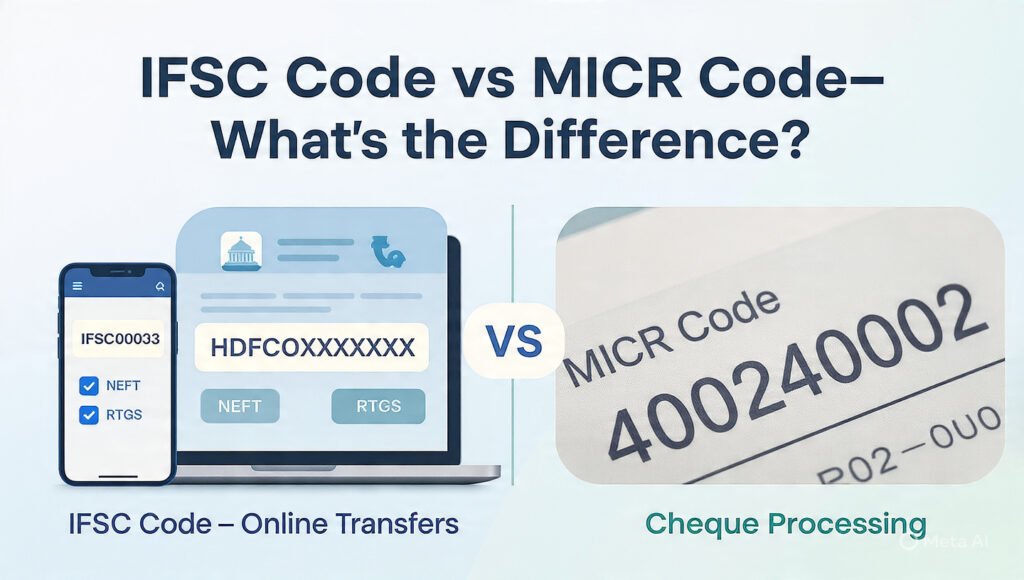

2. What is an IFSC Code?

The Indian Financial System Code (IFSC) is an 11-character alphanumeric string. Its primary purpose is to identify specific bank branches participating in the RBI-regulated electronic fund transfer systems.

Under the CTS-2010 standard, the IFSC is now a mandatory feature on all cheque leaves to facilitate modern banking. It is essential for:

- NEFT (National Electronic Funds Transfer)

- RTGS (Real Time Gross Settlement)

- IMPS (Immediate Payment Service)

The Anatomy of an IFSC

The code follows a strict logic mandated by the RBI:

- First 4 characters: Represent the Bank Name (e.g., SBIN for SBI, ICIC for ICICI).

- 5th character: This is always ‘0’ (zero). While often called a placeholder for future use, it acts as a crucial separator between the bank and branch identities.

- Last 6 characters: Represent the specific branch code.

Pro-Tip: While you need the IFSC to register a bank account on a UPI app for the first time, it is not required for daily UPI transactions, as they are handled via Virtual Payment Addresses (VPA) in the background.

——————————————————————————–

3. What is a MICR Code?

The Magnetic Ink Character Recognition (MICR) code is a 9-digit numeric identifier used primarily for the authentication and clearing of physical cheques. Unlike standard printing, MICR technology utilizes magnetic ink that is machine-readable. This is a critical safety feature: machines can accurately read the code even if the cheque is smudged, marked, or folded, significantly reducing the risk of human error.

The use of MICR enables Speed Clearing, a technology that leverages the National Clearing Cell of the RBI to facilitate automated cheque processing. This ensures that funds are moved far faster than traditional manual clearing methods.

The Anatomy of a MICR Code

The 9-digit format provides a geographical and institutional map:

- First 3 digits: City code (specifically aligned with the first three digits of the local PIN code).

- Middle 3 digits: Bank code.

- Last 3 digits: Branch code.

A major point regarding the difference between IFSC and MICR is their scope; while IFSC is an India-specific framework, MICR technology is a globally recognized standard for processing physical financial instruments.

——————————————————————————–

4. IFSC Code vs MICR Code – Key Differences

| Parameter | IFSC Code | MICR Code |

| Full Form | Indian Financial System Code | Magnetic Ink Character Recognition |

| Format | 11-character alphanumeric | 9-digit numeric |

| Primary Usage | Digital transfers (NEFT, RTGS, IMPS) | Physical cheque clearing & Speed Clearing |

| Mandatory For | Electronic Fund Transfers | Physical Banking Instruments |

| Technical Standard | CTS-2010 Standard | Automated Clearing Technology |

| Location on Cheque | Top (usually near branch address) | Bottom-center (right of cheque number) |

| Scope | India-specific | Globally recognized |

——————————————————————————–

5. Use Cases of IFSC Code

To ensure a seamless experience when you find IFSC code online, you should know exactly when it becomes the primary requirement. You will need it for:

- Setting up Online Transfers: Registering beneficiaries for domestic fund movements.

- Mutual Fund Investments: Authenticating Systematic Investment Plans (SIPs) or redemptions.

- Utility Bill Management: Paying high-value bills via net banking portals.

- Direct Benefit Transfers: Ensuring government subsidies reach the specific branch where your account resides.

——————————————————————————–

6. Use Cases of MICR Code

The MICR code meaning India is best understood through its role as the backbone of physical banking:

- Automated Cheque Clearing: Allowing specialized machines to route cheques to the correct bank and city instantly.

- Investment Authentication: When you submit a cancelled cheque for a new insurance policy or SIP, the MICR is used to verify the legality of the bank document.

- Interbank Settlement: Facilitating the final settlement of funds between different banks at the clearing house level.

——————————————————————————–

7. How to Find IFSC and MICR Code Easily (Recommended Method)

As an expert in the field, I recommend using a centralized database like ifsc.arjunwatchandmobile.com rather than searching through individual bank PDFs. This tool allows you to check bank details using IFSC and instantly retrieve the MICR code and branch address.

Step-by-Step Guide:

- Visit ifsc.arjunwatchandmobile.com.

- Enter your 11-digit IFSC code in the search field.

- Click Search.

- The system will display the Bank Name, Branch Address, and the associated 9-digit MICR code.

👉 Use our IFSC code finder to get complete bank details instantly: ifsc.arjunwatchandmobile.com

——————————————————————————–

8. Other Ways to Find These Codes

If you are away from the internet and cannot find IFSC code online, utilize these physical sources:

- Bank Passbook: The RBI mandates that banks print the IFSC and MICR on the first page of the passbook.

- Cheque Leaf: The IFSC is usually found near the top-left or top-right (close to the branch address). The MICR is located at the bottom-center, immediately to the right of the cheque number.

- Bank/RBI Directories: Official websites maintain exhaustive lists, though they can be cumbersome to navigate.

——————————————————————————–

9. FAQs

Is IFSC same as MICR? No. They have different formats and serve distinct stages of the banking process. IFSC is for electronic routing, while MICR is for machine-based physical clearing.

Can MICR be used for online transfers? No. MICR is not used for NEFT, RTGS, or IMPS. It is strictly for the clearing of physical instruments like cheques.

Where can I find MICR code? It is printed at the bottom of your cheque in a special magnetic font. You can also find it through our IFSC code finder.

Is the branch code same as the IFSC? Technically, no, but they are linked. The last six characters of any IFSC code represent that specific branch’s code.

Is IFSC required for UPI? It is required only for the initial account linkage/setup. It is not needed for individual peer-to-peer or merchant transactions.

——————————————————————————–

10. Conclusion

Understanding the technical nuances of banking identifiers is essential for the modern consumer. While the IFSC is the undisputed king of digital banking, enabling the speed of NEFT and RTGS, the MICR code remains the indispensable backbone of physical cheque processing.

Efficiency in banking depends on accuracy. According to RBI guidelines, cheque collection timelines are generally 7, 10, or 14 days for state capitals, major cities, and other locations respectively. To avoid unnecessary delays in these timelines, always ensure you provide the correct codes. Ensure your transaction reaches the right vault by verifying your details at ifsc.arjunwatchandmobile.com before finalizing any transfer!