Imagine you are standing in a car showroom, finally ready to pay for your dream SUV. The dealer expects a transfer of ₹15 lakhs immediately to confirm the booking. Or, perhaps it is the first of the month, and you need to ensure your landlord receives the rent, but it is not a life-or-death emergency if it arrives in a few hours. In another scenario, you might be out with friends and need to pay your share of a dinner bill instantly.

In the Indian banking ecosystem, these three scenarios require three different solutions: RTGS, NEFT, and IMPS. While all three move money from point A to point B, they are built on very different “payment rails.” Choosing the wrong one could mean your high-value business deal gets stuck in a batch or your urgent emergency fund arrives too late.

👉 Before transferring money, always verify bank details using our IFSC tool: ifsc.arjunwatchandmobile.com

——————————————————————————–

Understanding the Three Systems: A Story of Speed and Scale

To understand these systems, forget the technical jargon for a moment. Think of them as different ways to move cargo across a busy country.

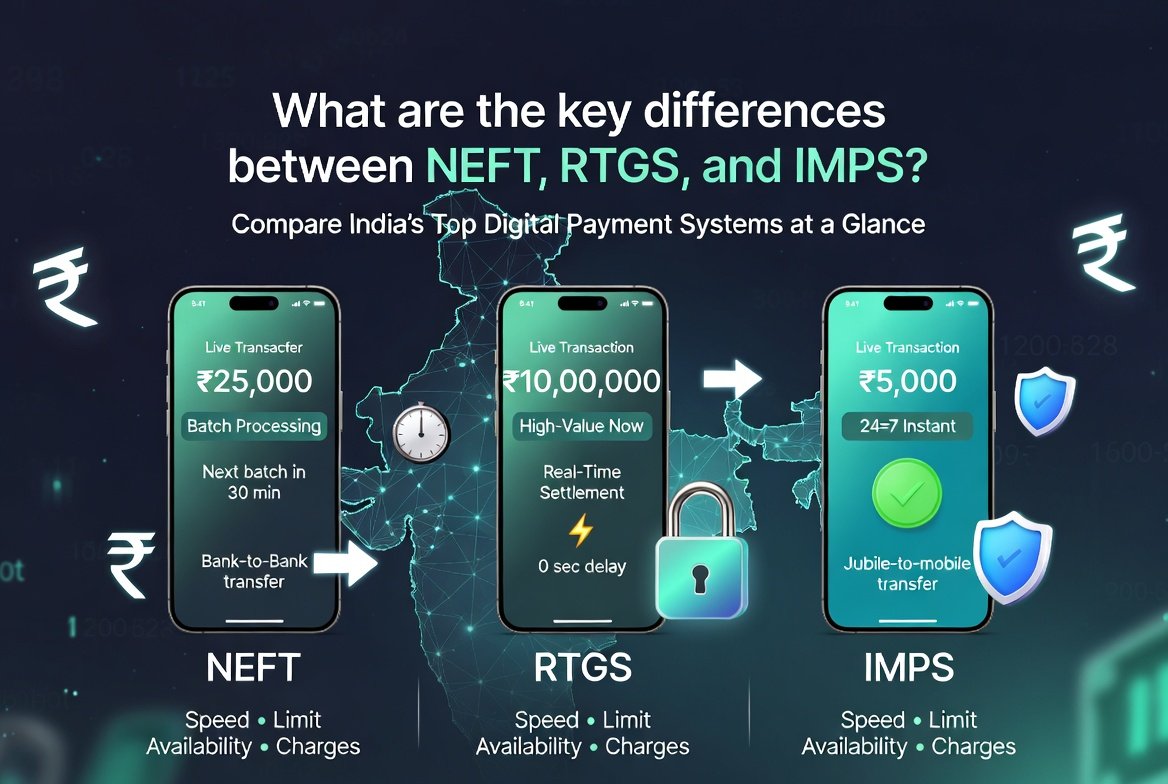

1. NEFT (National Electronic Funds Transfer): The Scheduled City Bus

NEFT is like a highly efficient city bus service. A bus doesn’t leave the station the moment one passenger sits down; it waits for a scheduled time, gathers everyone who arrived in the last 30 minutes, and then departs.

Owned and operated by the Reserve Bank of India (RBI), NEFT processes transactions in half-hourly batches. If you initiate a transfer at 10:05 AM, it won’t move until the 10:30 AM batch is cleared. It is a “credit-push” system, meaning only the person sending money can start the process. Because it moves in batches, it is technically a “hybrid” system—perfect for routine payments where a two-hour window for credit is perfectly acceptable.

2. RTGS (Real-Time Gross Settlement): The Private Express Highway

RTGS is the heavy-duty infrastructure of the Indian banking world. If NEFT is a bus, RTGS is a private express highway reserved for high-value cargo. The “Real Time” in its name means your instruction is processed the moment it is received, not held for a batch. The “Gross Settlement” part means each transaction is settled individually in the books of the RBI.

It is designed for speed and finality. Once an RTGS transfer is settled, it is final and irrevocable. Because it requires significant “liquidity” (available cash) from the banks, it is strictly reserved for large amounts—specifically starting from ₹2 lakhs.

3. IMPS (Immediate Payment Service): The Instant Drone Delivery

IMPS is the modern, digital-first answer to our need for “now.” While NEFT and RTGS were originally designed for traditional banking hours (though they are now 24/7), IMPS was built from the ground up to be instant.

It is like a drone delivery service that operates one-on-one. You send it, they get it—instantly. Managed by the National Payments Corporation of India (NPCI), IMPS is the backbone of most mobile banking apps. It is the go-to for daily retail needs where waiting for a “batch” to clear is not an option.

——————————————————————————–

Key Differences at a Glance

When deciding which method to use, this comparison table serves as a quick reference guide for Indian users.

| Feature | NEFT | RTGS | IMPS |

| Full Form | National Electronic Funds Transfer | Real-Time Gross Settlement | Immediate Payment Service |

| Settlement Type | Batch-based (Half-hourly) | Individual (Real-time) | Individual (Instant) |

| Minimum Limit | ₹1 | ₹2 Lakhs | ₹1 |

| Maximum Limit | No RBI limit | No RBI limit | ₹5 Lakhs (standard) |

| Speed of Credit | Up to 2 hours | Within 30 minutes | Instantaneous |

| Availability | 24/7/365 | 24/7/365 | 24/7/365 |

| Managed By | RBI | RBI | NPCI |

| Best Use Case | Salaries, Rent, EMI | Property, Business Deals | Emergencies, Daily use |

——————————————————————————–

When Should You Use Each? Practical Scenarios

Choosing the right payment rail is about balancing urgency with the amount being sent.

Use NEFT When:

- You are paying a recurring bill: If you are paying your monthly house rent or a utility bill, the half-hour batch delay doesn’t matter.

- You are a business owner paying salaries: NEFT is the most economical way to move money to dozens of employees at once.

- You are paying Credit Card dues: NEFT is widely used for card bill payments by using the 16-digit card number as the account number.

- The amount is small to medium: There is no upper limit, but for non-urgent transfers, NEFT is the standard.

Use RTGS When:

- You are buying a car or property: Since the minimum limit is ₹2 lakhs, it is the safest way to move large sums with the “legal backing” of the RBI.

- Settlement finality is critical: In large business deals, “Real-Time” settlement reduces the risk that a payment might be reversed or stuck in a backlog.

- You need proof of credit quickly: RTGS beneficiary banks must credit the account within 30 minutes of receiving the message.

Use IMPS When:

- You are in an emergency: If a friend needs money for a hospital bill or a travel ticket, IMPS is the only one that guarantees the recipient sees the “Amount Credited” notification immediately.

- It is a weekend or bank holiday: While NEFT and RTGS are now 24/7, some older bank systems still handle IMPS more smoothly during non-business hours.

- You don’t have the recipient’s full details: IMPS often allows transfers using just a mobile number and MMID, though using an account number and IFSC is more common.

——————————————————————————–

The Critical Role of the IFSC Code

Regardless of whether you choose NEFT, RTGS, or IMPS, there is one piece of data that acts as the “GPS” for your money: the IFSC (Indian Financial System Code).

The IFSC is an 11-digit alphanumeric code. The first four characters represent the bank, the fifth is always a zero, and the last six identify the specific branch. Without a valid IFSC, the “Processing Centre” (operated by the RBI for NEFT/RTGS) cannot route your message to the correct destination.

The Risk of the Wrong IFSC: If you enter an incorrect IFSC, your money could end up in a “gridlock” or be returned to your account after a delay. In a worst-case scenario, if the account number exists in another branch with that wrong IFSC, the money could be credited to the wrong person. Banks are required to credit funds solely based on the account number, making the IFSC and account number combination your most vital responsibility.

👉 Use our IFSC code finder to get bank name, branch address, and MICR instantly.

——————————————————————————–

Common Mistakes Users Make

- Trying to send ₹1 Lakh via RTGS: Users often get frustrated when their banking app doesn’t show the RTGS option. Remember, the “highway” is closed for anything under ₹2 lakhs. Use IMPS for instant credit or NEFT for a batched transfer.

- Using NEFT for Urgent Deadlines: If you have to pay a school fee by 4:00 PM and you initiate an NEFT at 3:55 PM, it might not clear until 4:30 PM. Always account for the half-hourly batch cycles.

- Ignoring GST on Charges: While the RBI has waived processing charges for banks since July 2019, and online NEFT is free for savings account holders, banks may still charge for offline (branch) transactions. These charges often attract an 18% GST.

- Incorrect Beneficiary Addition: Most banks have a “cooling-off” period (often 30 minutes to 2 hours) after you add a new beneficiary before you can send a large amount. Plan your transfers ahead of time.

——————————————————————————–

Which One is Best? The Quick Decision Guide

If you are still undecided, follow this simple logic flow:

- Is the amount ₹2 Lakhs or more?

- Yes, and it’s urgent? → RTGS

- Yes, but I can wait an hour? → NEFT

- Is the amount less than ₹2 Lakhs?

- Yes, and I want it there now? → IMPS (Up to ₹5 Lakhs)

- Yes, and a small delay is fine? → NEFT

- Is it for a person who doesn’t have a bank account?

- Yes? → NEFT (Cash deposit at a branch is allowed up to ₹50,000).

——————————————————————————–

FAQs (Human Style)

Which is fastest: NEFT, RTGS, or IMPS? IMPS is the fastest for small to medium amounts (instant). RTGS is the fastest for large amounts (real-time). NEFT is the slowest because it moves in 30-minute batches.

Is IFSC required for all three? Yes. Whether you are using the RBI’s “city bus” (NEFT) or the “express highway” (RTGS), the IFSC is the address the system uses to find the right branch. You can check bank details using IFSC on our portal.

What happens if my NEFT is not credited? If a beneficiary’s account cannot be credited for any reason (like a wrong account number), the destination bank must return the money to the sender within two hours of the batch’s completion. If they delay, they are liable to pay penal interest (Repo Rate + 2%).

Can I use IMPS for big transactions? IMPS is generally capped at ₹5 Lakhs per day. If you need to send ₹10 Lakhs, you must use RTGS (for instant) or NEFT (for batched).

——————————————————————————–

Conclusion

Understanding the difference between NEFT, RTGS, and IMPS is about more than just knowing bank acronyms; it’s about financial literacy. In a world of digital payments, being “smart” means knowing that NEFT is for your routine schedules, RTGS is for your big life milestones, and IMPS is for your immediate needs.

The Indian banking system, governed by the RBI, has made these tools available 24/7/365 to ensure that “liquidity” flows smoothly across the country. However, the system is only as accurate as the data you provide. A single digit wrong in an account number or a typo in an IFSC can lead to failed transactions and unnecessary stress.

👉 Always double-check your IFSC before transferring money. Find bank branch details online using our quick and accurate tool for a worry-free transfer.

——————————————————————————–

Related Articles for Further Reading:

- NEFT Explained: A deep dive into batch settlements.

- RTGS Guide: How the RBI handles large-value transactions.

- IMPS Article: Why it’s the king of mobile banking.

- IFSC vs MICR Code: Which one do you actually need?